Business Online Banking Security

New financial standards will assist banks and business account holders to make online banking safer and more secure from account hijacking and unauthorized funds transfers.

As someone responsible for a business bank account, you will want to know that new supervisory guidance from the Federal Financial Institutions Examination Council (FFIEC) are helping banks strengthen their vigilance and assure that your business accounts are properly secured during money transfers of all kinds. FFIEC is the coordinating group that sets standards for the major financial industry regulators and examiners.

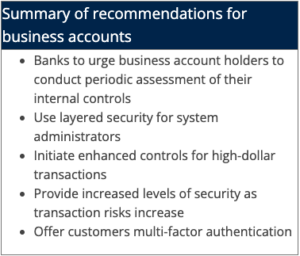

FFIEC studies have shown that there have been significant changes in the threat landscape in recent years. Fraudsters—many from organized criminal groups—have continued to deploy more sophisticated methods to compromise authentication mechanisms and gain unauthorized access to customers’ online accounts. For example, hacking tools have been developed and automated into downloadable kits, increasing their availability to less experienced fraudsters. As a result, online account takeovers and unauthorized funds transfers have risen substantially each year since 2005, particularly with respect to commercial accounts, representing losses of hundreds of millions of dollars. The FFIEC supervisory guidance addresses the fact that not every online transaction poses the same level of risk, recommending that financial institutions implement more robust controls as the risk level of the transaction increases. Online business transactions generally involve ACH file origination and frequent interbank wire transfers. Since the frequency and dollar amounts of these transactions are generally higher than consumer transactions, they pose a comparatively increased level of risk to the institution and its customer, according to FFIEC. Thus banks are advised to implement security plans utilizing controls consistent with the increased level of risk for covered business transactions. These enhanced controls are designed to exceed the controls applicable to routine customer users. For example, a preventive control could include requiring an additional authentication routine prior to final implementation of the access or application changes. A detective control might include a transaction verification notice immediately following implementation of the submitted access or application changes. Based upon the incidents the Agencies have reviewed, enhanced controls over administrative access and functions can effectively reduce money transfer fraud. Layered security is characterized by the use of different controls at different points in a transaction process so that a weakness in one control is generally compensated for by the strength of a different control. This allows your bank to authenticate customers and respond to suspicious activity related to initial login…and then later to reconfirm this authentication when further transactions involve the transfer of funds. For business accounts, layered security might often include enhanced controls for system administrators who are granted privileges to set up or change system configurations, such as setting access privileges and application configurations and/or limitations.

The new supervisory guidance offers ways your bank can look for anomalies that could indicate fraud. The goal is to ensure that the level of authentication called for in a particular transaction is appropriate to the level of risk in that application. Accordingly, your bank has concluded a comprehensive risk assessment of its current methods as recommended in the FFIEC guidelines. These risk assessments consider, for example:

Your bank joins FFIEC and the financial regulatory agencies in strongly urging businesses account holders to conduct similar internal assessments to ensure the highest level of security possible for your transactions.

Whenever increased risk to your transaction security might warrant it, your bank will have available additional verification procedures, or layers of control, such as:

Banks follow specific rules for electronic transactions issued by the Federal Reserve Board known as Regulation E. Under the protections provided under Reg E, consumers can recover internet banking losses according to how soon they are reported. In general, these protections are extended to consumers and consumer accounts.

If you notice suspicious activity within your account or experience security related events (such as a Phishing email from someone purporting to be from your bank), you can contact us at 301-898-4000 and you will be quickly and courteously guided to the person responsible for such issues.

Business Online Banking Security

Risk Assessment & Layered Security

Banks and businesses team up for security

Understanding The Risks

Enhanced Controls Protect Higher Risks

Layered Security For Increased Safety

Your bank uses both single and multi-factor authentication, as well as additional “layered security” measures when appropriate.

Your bank uses both single and multi-factor authentication, as well as additional “layered security” measures when appropriate.

Internal Assessments At Your Bank

Examples of Layered Security For Business Accounts

Your Protections Under “Reg E”

By continuing, you will be leaving the Woodsboro Bank's website and entering a website hosted by another party. Woodsboro Bank does not assume liability for the content, information, security, policies or transactions provided by other sites.